Accounting for your eCommerce business? It is amongst the most painful yet prerequisite to sustain your eCommerce business the right way.

It may seem uninteresting to business owners. Instead, they engross themselves in thinking to expand their product line. But in reality, having a basic knowledge of accounting for your eCommerce business is a must-have to carry out a successful business.

If we look at the stat by NetSuite, eCommerce retail is, by the year 2024, forecasted to reach a point of $6.5 trillion in purchases, factoring in 22% of all global retail sales.

Provided that you have a grip on the fundamentals of accounting, you will be adequately intelligent to figure out what the numbers tell you. Alternatively, you can also Hire a Professional Accountant near you who can ready up all your accounting-related tasks in no time.

Underneath, I have shed light on the Top 10 Ecommerce Accounting Tips & Best Practices for 2022.

Top 10 Ecommerce Accounting Tips & Best Practices for 2026

#1 Keep Watch Over Your Cash Flows

To make this simpler, what is the principal goal of any eCommerce business? To raise money, Right? And an even important thing is to know where your money is coming from and going to – keeping a close watch on the cash flow.

To keep track of your finances, always opt for a reliable business accounting software like Zoho Books. Read this review of Zoho Books to see if the tool is a great fit for your business accounting needs.”

Put a strategic plan, make payments on time. Also, make notes of the timing of your cash flow – What is the due date of your receivables and bills? When is the time to pay your employees?

- Monitor your cash flow weekly! If the cash coming and going out is incomparable, you can know in real-time that you are in trouble.

- Pay your bills only on the due date – not before.

- Store some cash in your bank account. It will help you in urgency.

#2 Manage Your Inventory

Inventory – the goods you sell and the materials used to produce that good. This also includes costs incurred to package the goods.

Unnecessarily building inventory impacts directly on your cash and affects inadequately on your assets. Hence, keeping your inventory under control is an indispensable part, and decide a minimum volume for it.

A guideline is to keep only that much that you need.

Try not to run out of inventory and also do not make it in excessive amounts.

#3 Understand your cost of goods sold

The caused cost when producing a good that is to be sold is the cost of google sold. This also includes labor costs and the raw materials’ costs used in producing the item. What is not included in this is the expenditure on distributing and selling the goods.

Use the weighted-average method or specific identification method to calculate your cost of goods sold.

Monitoring the cost of goods sold correctly is imperative as these figures play a decisive role in finding accurate financial reports.

#4 Calculate other expenses.

In addition to the cost of goods sold, there comes fixed costs. It is the cost that is bound to happen no matter if you sell items or not.

- Rent & Utilities

- Insurance

- Property Tax

- Interest on loan payments

- Salaries

#5 Calculating the Break-Even Point

The break-even point refers to a point where your revenue equalizes your costs. When you hit this point, Your profit rate will stand at zero level. Simply put, you have succeeded to meet your costs with the generated sales.

To calculate the break-even point implies calculating your fixed and variable costs, product prices, and contribution margin.

Contribution price is obtained when deducting your variable costs from the sale price. Use the subsequent formula to estimate your break-even point.

Break-even Point = Fixed Costs/Contribution Margin

#6 Track your profits before tax

The next stage is to figure out your sales rates. So that, you can know in advance whether you are on the right path to arrive at your targeted revenue or not. This will also help you to distribute money in various business operations.

One best practice to monitor your business’s sales is to connect your website with Google Analytics.

To know your profits before tax, just subtract your cost of goods sold, functioning costs, and your interest rate from total income.

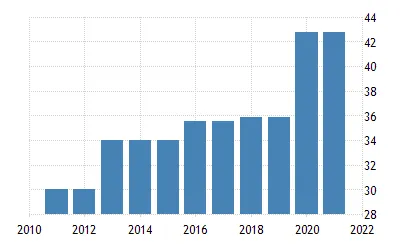

#7 Proper Tax Rates

Next up is the taxes – the thing that most people grumble on.

but tax rates are both inevitable and complex. When a consumer buys a product. You are obligated to provide them with the product with the payable tax.

For best practices, classify products according to the ones that require tax and ones that are free from taxes.

Image Source – Trading Economics

Image Source – Trading Economics

#8 Tax payments

Once you have gathered taxes from the products, you need to guarantee that you are ready to pay them. The tax rules depend on your location. When starting, expect payable tax the same as the tax you have received from the customers.

It is imperative to understand the temperament of your taxes and not include them as a portion of your revenue. If this is not made, you will face issues when it is time to make restitution.

#9 Balance Sheet

Now that everything is wrapped including your earnings and cash flow, the last element to look after is the balance sheet.

A balance sheet is largely for following the long-term well-being of your firm and to understand how it is performing. The balance sheet comprises assets, liabilities, and equity.

Assets – everything you have of value, like money.

Liabilities – debts you owe.

Equity – the interval between the above two.

Note – if assets = liabilities + owner’s equity, then and only then your balance sheet is true.

#10 Buy yourself an accounting software

Do not try to bury it all down together on an excel sheet or using a calculator.

The best bet is to get accounting software.

To rationalize the accounting method, firms should spend on basic software tools. Managers can pick from various e-commerce accounting platforms. Intuit Quickbooks, FreshBooks, Zoho Books, etc.

Wrap Up!

Okay, these are the basics of accounting you need to keep track of, routinely.

To begin with, buy accounting software that can make your life a whole lot easier. Thereafter, keep control of the cash flow which should be managed weekly.

Next, you require to recognize your sellouts, costs, and gains. Remember to plan for taxes. Lay the tax money alongside to pay them when it is actually needed. Lastly, prepare a balance sheet.

Happy Reading!

This is a great blog post on how to hire a good hire keeper; thank you for posting this.

You make a great point about making sure you monitor cash flow through sheets. I need to get a software package to help with streamlining processes. I’ll have to consider getting NetSuite.

Great tips and ideas that business owners can follow through it.

Wow, this blog is fantastic. I love reading your articles. Keep up the good work! You realize that many individuals are searching around for this info, and you could aid them greatly.

Thank you for sharing. It is really interesting tips.

Great blog sharing practical ecommerce accounting tips, best practices, and smart strategies to improve profits, accuracy, and business financial management.